Our website has detected that you are using an outdated browser that will prevent you from accessing certain features. An upgrade is recommended to improve you browsing experience.

The SARB was established on 30 June 1921 to issue, distribute and destroy banknotes and coin. The first banknotes were issued by the SARB on 19 April 1922.

The rand has been legal tender in South Africa since 1961, when it replaced the pound. It takes its name from the Witwatersrand – the ridge on which Johannesburg is built and where most of South Africa’s gold deposits were found.

The rand is legal tender in the Common Monetary Area, which includes, eSwatini, Lesotho and Namibia.

In 1996 the mandate of the SARB was expanded to include price stability maintenance, one of its main functions remains ensuring a sufficient supply of trusted banknotes and coin.

The Currency Management Department works with the South African Mint Company (RF) Proprietary Limited (SA Mint), which mints coins, and the South African Bank Note Company (RF) Proprietary Limited (SABN), which prints banknotes. Both are subsidiaries of the SARB.

The SARB Act 90 of 1989 provides for the legal tender status of the banknotes and coin issued by the SARB. It also contains provisions relating to the mutilation, reproduction and counterfeiting of South African banknotes and coin.

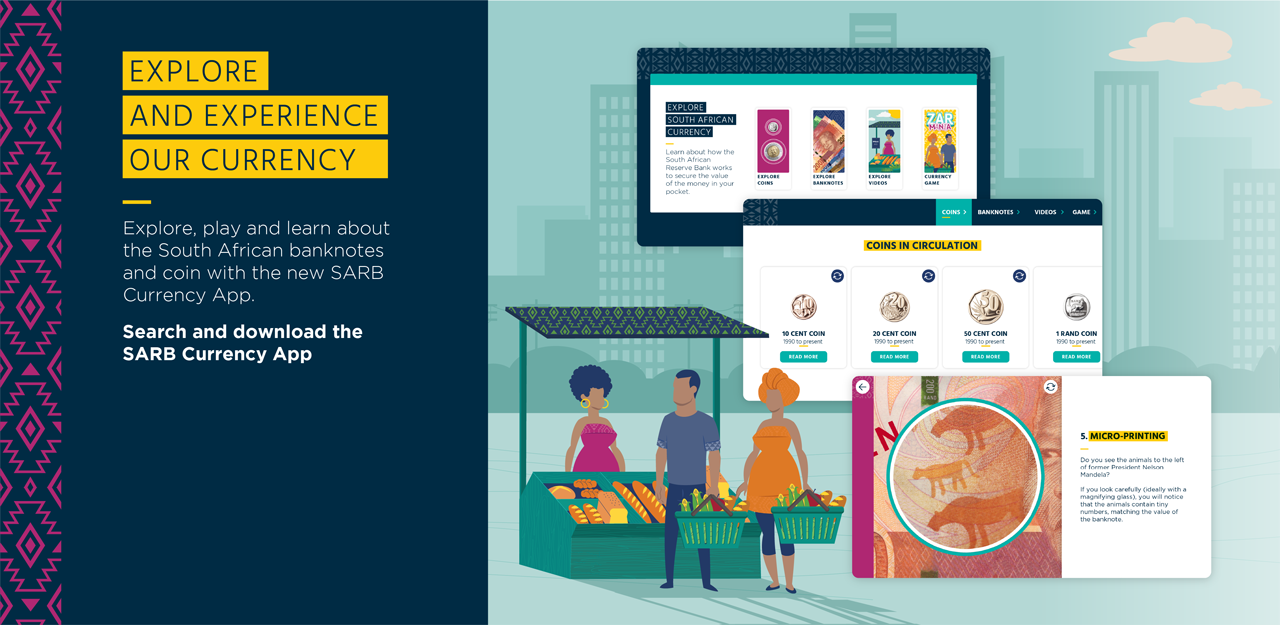

Our app encourages users to explore, learn and discover everything about South African banknotes, including commemorative banknotes. From the inspiration behind both Mandela series and commemorative banknote, to their technical, design and security features, the app will take you on a fun, educational journey across South Africa’s banknote landscape.

The reverse of the commemorative banknotes can be scanned to experience the life story of Nelson Mandela, from his humble beginnings in the Eastern Cape to the moment he was inaugurated as South Africa’s first democratically elected president. The app allows users to access the stories on all banknotes even if they only have one commemorative banknote to scan. Another feature on the app is the “play the banknotes” challenge, where users can try to beat the clock by testing their knowledge of South Africa’s banknotes then share their results on social media.

The SARB acts proactively by developing new banknotes to ensure that the country’s money remains among the most trusted currencies in the world. This is done to ensure continued relevance of the design and to incorporate technological advances, ensuring trust is maintained in the currency.

A number of design objectives are considered when designing and developing new banknotes and coin that:

R200 plates ready for printing

The Kruger Rand moulding

The Currency Management Department works with its subsidiaries namely, the South African Mint Company (RF) Proprietary Limited (SA Mint), which mints coins, and the South African Bank Note Company (RF) Proprietary Limited (SABN), which prints banknotes. Both are subsidiaries of the SARB.

The SARB forecasts and calculates annually the volume of banknotes and coin needed to meet public demand. The production and technical teams decide on the technical, quality and security features of the banknotes and coin. The SABN and SA Mint then produce the new banknotes and coin based on the annual order placed.

R100 banknotes sheets in production

The coin cleaning process

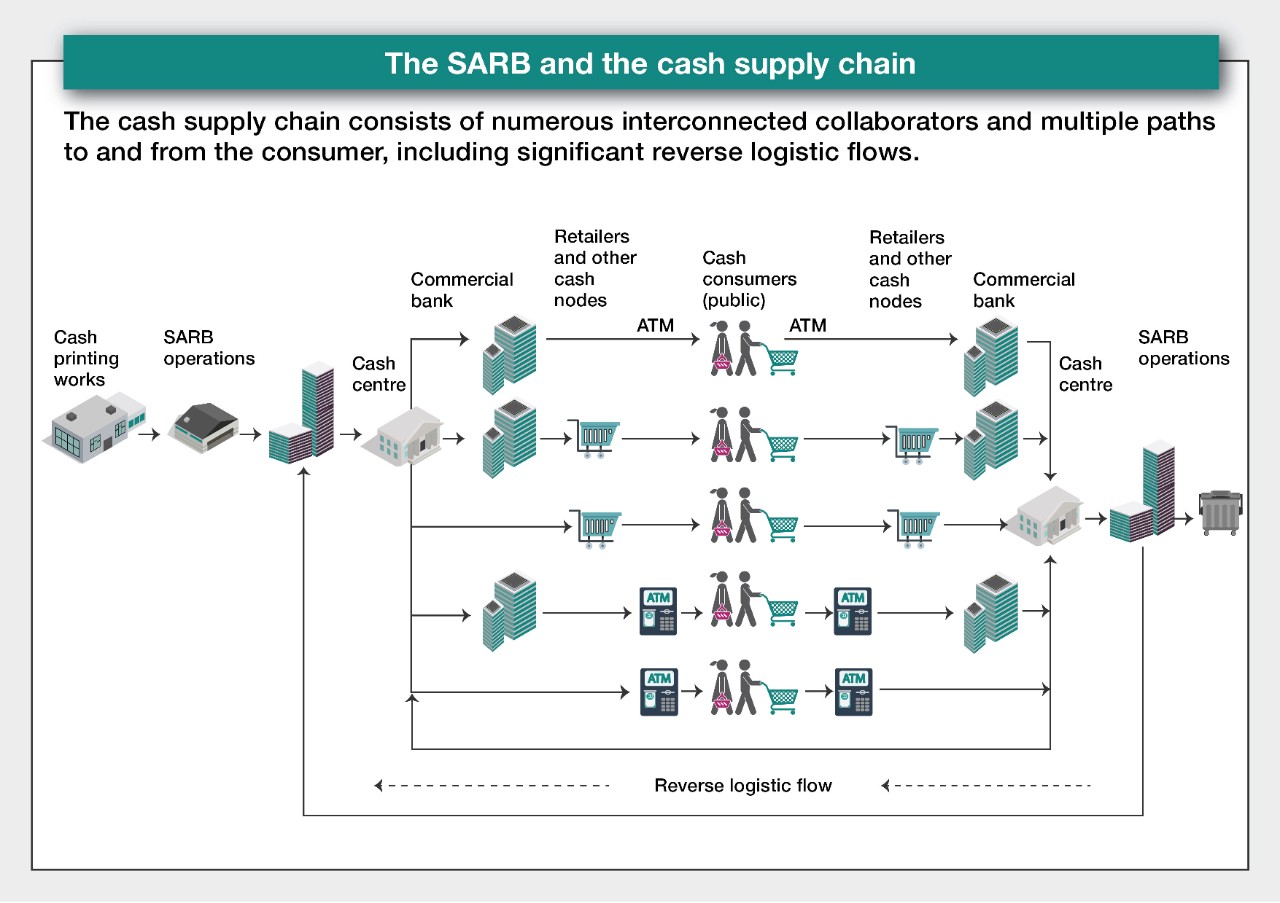

The SARB ensures the availability and adequacy of banknotes and coin throughout the country in line with section 10(1)(a)(i)–(v) of the SARB Act. It is responsible for the bulk issuance and distribution of banknotes and coin and for meeting public demand for cash.

The Currency Management Department is responsible for managing and overseeing the cash supply chain, from planning, distribution and issuance, to destruction of cash.

Printed banknotes are transported from the subsidiary to cash centres for issuance to commercial banks. The SARB’s cash centres are located in Johannesburg, Durban and Cape Town and are not open for transactions with the public.

Commercial banks hold sufficient banknotes and make them available at their branches and automated teller machines (ATMs), where they can be withdrawn and used for transactions by the public.

A CBDC can be defined as a form of money that is denominated in fiat currency[1] (central bank money), in an electronic form, and which is a liability on the central bank’s balance sheet similar to cash and central bank deposits. In the context of SARB’s current CBDC feasibility study, it could be considered as “smart cash” with unique attributes enabled by its digital form.

The Bank for International Settlements[2] (BIS) defines a CBDC as a purely digital banknote that could be used by individuals to pay businesses, shops or each other (called a "retail CBDC"), or between financial institutions to settle trades in financial markets (called a "wholesale CBDC").

The objective of the study is to investigate if it would be feasible, appropriate and desirable for the SARB to issue a CBDC to be used for retail purposes, complementary to cash in South Africa.

No. The outcome of the feasibility study will reveal the desirability and appropriateness of issuing a CBDC in South Africa. It will highlight the different CBDC design options and the potential policy and/or regulatory implications associated with these options. The insights gained will inform the decision around whether to pursue the issuance of a South African CBDC.

Even if the outcome of the feasibility study suggests that the issuance of a CBDC in South Africa may be feasible and/or desirable, it does not necessarily imply that it will be pursued.

Cash has a physical presence, whereas a CBDC is available exclusively in digital format. The digital nature of a CBDC unlocks potential benefits related to usability for consumers and merchants, safety and security, and traceability of transactions without infringing on privacy rights. CBDC payments and remittances can be made remotely, which is harder to do with cash.

Crypto assets are privately issued (i.e. by a non-central bank) and have a decentralised and disintermediated value proposition (i.e. crypto assets offer a direct, peer-to-peer transactional capability that does not require a financial intermediary, such as a bank). Crypto assets are not a liability on any institution’s balance sheet and unlike a CBDC, they are not backed by any government or centralised authority. Because they are not on anyone’s balance sheet as an obligation to the holder (i.e. the holder has no claim on the issuer as there is no central issuer), the user is potentially exposed to risk. Crypto assets such as Bitcoin are susceptible to large price fluctuations, generally making them less predictable and therefore less suitable as a stable medium of exchange.

The introduction of a more stable type of crypto asset, known as “stablecoins”, addresses the inherent volatility of crypto assets by linking the value of the crypto asset to a fiat currency (such as the US dollar), a basket of fiat currencies (such as US dollar, euro and others), or a traditional asset or commodity (such as gold or oil).

In short, if a CBDC is guaranteed by the issuing central bank, it would be as safe as cash and would have minimal or no counterparty risk.

When money is held in a commercial bank account in a digital form, it represents an amount owed to you by that bank; in other words, it is a claim that you have against the bank. It can typically be withdrawn in its physical form, but only if the bank is solvent. A CBDC, on the other hand, is backed by the central bank and is a liability on the central bank balance sheet, similar to cash. A CBDC with legal tender status would not be a commercial bank’s liability, so you would not have to rely on a particular bank’s solvency to be able to maintain your balance.

The focus of the SARB’s CBDC feasibility study is on a retail CBDC, that is, a CBDC that is accessible to the general public for everyday consumer and merchant commercial activities. By contrast, a wholesale CBDC is typically available only to financial institutions for high value transactions.

The core principles applicable to the design features of a CBDC in

South Africa are as follows:

In addition to these core principles, the following attributes of a CBDC should be addressed in its design:

The CBDC feasibility study will examine two types of deployment models, typically considered globally. These can be summarised as:

The CBDC feasibility study is expected to examine the advantages and disadvantages of both models.

A ledger is basically a record system. DLT is a secure digital system for recording the transacting of assets (such as CBDC) in which the transactions and their details are recorded in multiple places simultaneously. This approach offers benefits in terms of resilience (less exposure to a central database failure), as well as safety and integrity through validation of transactions by multiple stakeholders.

Blockchain technology is used to facilitate a shared, distributed and immutable ledger. The term “immutable” refers to the attribute of a blockchain that ensures that the integrity of the history of every transaction that has ever occurred can be guaranteed. The name comes from the way transactions are grouped into blocks, verified, processed and stored in a sequence (chain) that is electronically verifiable, which makes it indisputable.

Bitcoin is an example of a crypto asset developed using blockchain technology.

DLT can be seen as a family of technologies, ranging from distributed databases to tokenisation, while blockchain is one type of this technology.

There is no fixed rule regarding the technology used to implement a CBDC. It is more important that the requirements and design attributes are understood before selecting a technology that solves these needs. However, most existing CBDC projects are based on a form of DLT, or a “blockchain-like” technology.

Yes. Should a CBDC be issued, the most likely scenario is that it would exist alongside cash, so that people can decide whether they want to use cash, the CBDC, commercial bank money, or some combination of these. Therefore, much the same as physical cash co-exists with money in your bank account, and can be transferred from one form of money to another, a CBDC would provide another option with its own unique qualities.

A digital wallet can be described as a container (i.e. an electronic device) in which the holder may securely store digital value. Potential consumer devices include chip-embedded cards, smartphones, and a number of emerging dedicated devices incorporating additional security features such as biometric readers or PIN codes.

Digital wallets typically include technologies to interface with point-of-sale devices, such as QR code scanners, near-field communications and other wireless communication technologies, thereby providing a secure means of transacting and transferring value between consumers and businesses.

No; according to a recently published BIS survey,[1] the year 2020 saw an official launch of a retail CBDC in the Bahamas; it is likely that more will be rolled out soon. Most central banks are exploring the case for CBDCs. Overall, the survey indicates a continuous move from purely conceptual research to experimentation and pilot projects. Yet despite these developments, a widespread roll-out of CBDCs still seems some way off.

The CBDC feasibility study will examine the extent to which a CBDC would support a number of outcomes potentially affecting the SARB, the national payment system, as well as consumers and businesses. The study topics include:

The CBDC feasibility study will consider potential risks and unintended consequences and how these would need to be mitigated. Some of these are:

A retail CBDC is not intended to displace or compete with other payment instruments. Rather, it is a potential additional payment instrument with specific attributes and characteristics that make it attractive for certain uses.

[1] Fiat currency is a government-issued currency.

[2] https://www.bis.org/about/bisih/topics/cbdc.htm

[3] C Boar and A Wehrli, ‘ Ready, steady, go? – Results of the third BIS survey on central bank digital currency.’ BIS Papers No 114. BIS Monetary and Economic Department, January 2021. https://www.bis.org/publ/bppdf/bispap114.ht3

There are five denominations of South African banknotes in circulation: R10, R20, R50, R100 and R200.

All South African banknotes are printed on cotton substrate and can be differentiated from one another by considering the dominant colour, animal theme and size.

All banknotes and coins issued since 1961, by the SARB, remain legal tender in South Africa. To see these past banknotes, please see The history of banknotes and coin in South Africa.

There are six denominations of South African coin in circulation: 10c, 20c, 50c, R1, R2 and R5. The minting of the 1c, 2c and 5c having been discontinued.

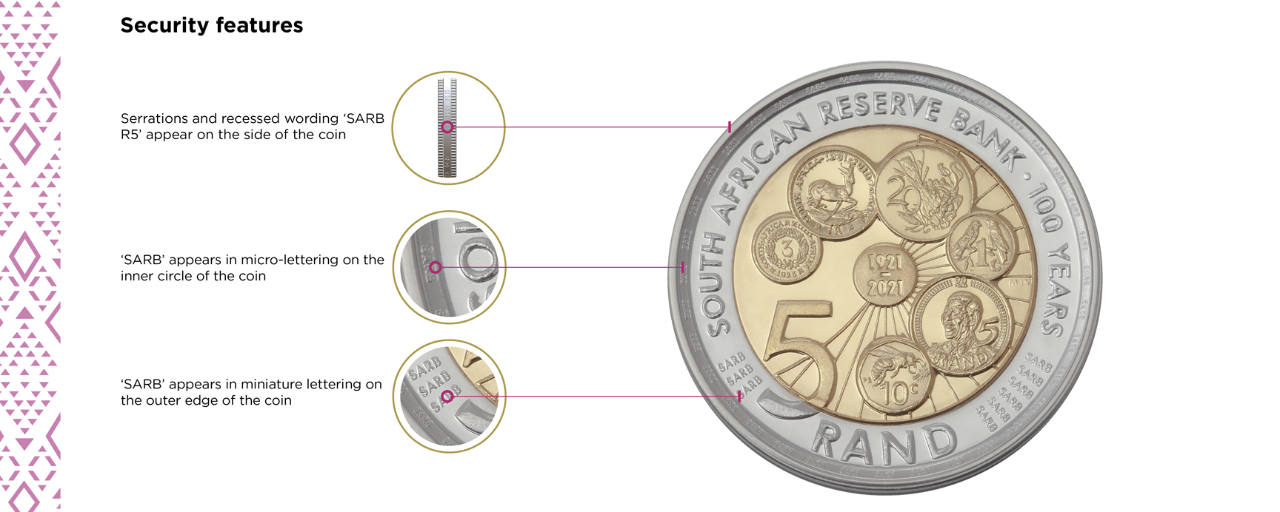

All South African coins are minted on combinations of base metals and alloys and can be differentiated from one another by their size, dominant colour, theme on the reverse, and the ridges, rims and serrations on their edges.

1990 to present

1990 to present

1990 to present

1990 to present

1989 to present

2005 to present

In addition to the above coins, the SARB issues commemorative coins from time to time. For further information on these coins and their value, please see Commemorative Coin below.

All banknotes and coins issued since 1961, by the SARB, remain legal tender in South Africa. To see these past coins, please see The history of banknotes and coin in South Africa.

This coin celebrates the 90th anniversary of the South African Reserve Bank.

This coin celebrates 20 years of constitutional democracy in South Africa

This coin marks the 200th anniversary of the first known currency created in South Africa.

This coin celebrates 100 years since the birth of Oliver Tambo (1917 -2017).

This coin celebrates 100 years since the birth of Nelson Mandela ( 1918 - 2018).

The long line of voters represents the desire of citizens to participate in shaping the future.

This coin celebrates 25 years of constitutional democracy in South Africa and recognises the people of the nation who live and strive for freedom.

These coins display designs and themes which are different from our normal circulation coins, but despite their limited circulation volumes and intended use as a commemorative circulation coin, they maintain their face value over time.

This coin depicts the essence of joy, which all children should experience. It reminds us that all children in our nation are entitled to equal protection and should be able to exercise their rights.

This coin celebrates the potential of education to transform the lives of people of all ages. The building block, open book and graduation cap represent the importance of early learning, access to quality schooling and higher education.

All South Africans share the right to access unspoiled natural resources. This coin depicts some of the resources we need for our survival, like safe water, food and air.

The raised hands in different gestures symbolise the diversity of individual opinions and the wish to be heard. This coin recognises the right of every person to choose, practise and change their religion and beliefs.

The bird holding a key represents the right of all South Africans to freedom of movement. The taxi and aeroplane show that we have the right to choose our place of residence, to travel and be welcomed home.

This coin depicts the 25 years of Constitutional Democracy in South Africa

Hence, despite the beauty of these coins or emotional connection they might hold to the commemorative topic, they should not be kept with the expectation that they will increase in value.

It is therefore prudent to be wary of anyone offering to pay significant amounts for these coins.

It is the responsibility of the SARB to ensure and maintain the integrity of banknotes and coin in circulation. The SARB has to ensure that banknotes and coin remain a secure method of payment, unit of account and store of wealth. Banknotes and coin derive their value from the trust that the citizens have in that country’s currency.

It is important to be aware of the security features incorporated in banknotes in order to identify counterfeit notes. When inspecting banknotes an approach of Look, Feel, and Tilt should be adopted.

By holding a banknote up to the light, the following features can be observed.

The security thread is the shiny strip on the front of the banknote, which becomes a continuous solid line when held to the light. The words “SARB”, “Rand”, the denomination and the South African coat of arms should be visible.

The watermark is an embedded image of Nelson Mandela with the denomination.

By lightly running your fingertips over the banknote, the following features can be observed.

On the front of the banknote, the portrait of Nelson Mandela and the words SOUTH AFRICAN RESERVE BANK will feel slightly raised or rough.

The raised lines on the bottom left and right of the front of the banknote are aids for the visually impaired. The R10 has one line, the R20 two lines, the R50 three lines, the R100 four lines and the R200 five lines.

By tilting a banknote, the following features can be observed.

The metallic thread will reflect light and exhibit a slight colour shift.

The numerals on the bottom right of the banknote are printed with a colour-changing ink. The R10 and R20 banknotes exhibit a slight colour shift, whereas the R50, R100 and R200 banknotes appear to have a moving line. If you suspect that you have a counterfeit note, see Counterfeit Notes below.

In terms of section 14 of the SARB Act, only the SARB has the right to issue banknotes and coin in South Africa. Any reproduction of banknote images – even for artistic or advertising uses – is strictly forbidden.

Counterfeit currency are imitation notes or coin produced without the legal sanction of the SARB. Counterfeiting currency and the possession thereof are crimes.

By law, counterfeit notes found in circulation cannot be exchanged for cash, as they have no value. To confirm the validity of a banknote, the approach of Look, Feel and Tilt can be used.

The SARB, the South African Police Service and the commercial banks work together to combat the counterfeiting of banknotes and coin. Members of the public who come into possession of counterfeit banknotes and coin must immediately report it to their nearest police station.

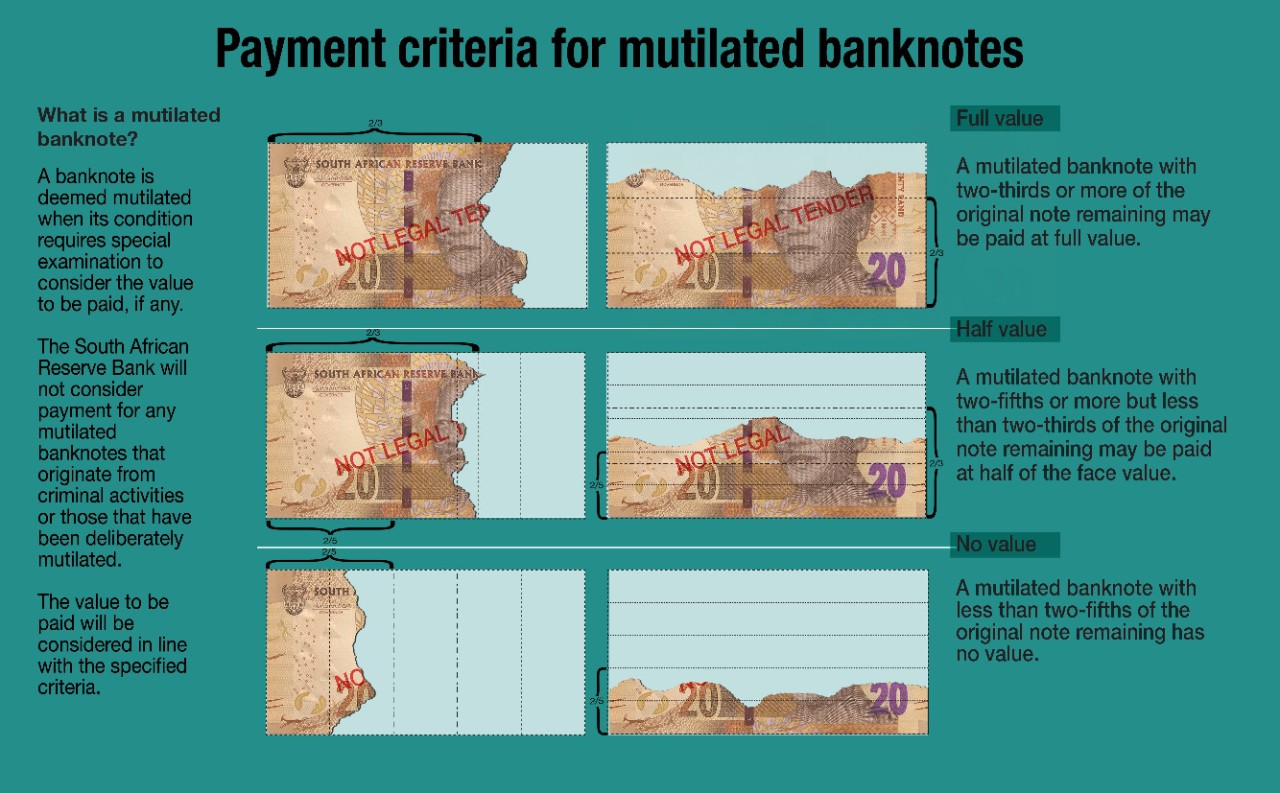

A banknote is deemed mutilated when its condition requires special examination to validate. Such banknotes could be burnt, discoloured, decomposed, or damaged with portions missing.

In terms of section 14(4) of the SARB Act, the SARB is not obliged to make any payment in respect of mutilated banknotes, but will consider the merits of each case. As such, mutilated banknotes may be exchanged at the SARB Head Office in Pretoria or designated commercial bank branches, where the value to be paid will be evaluated against specific criteria.

Mutilated banknotes can also be exchanged at a commercial bank where an individual’s account is held. Designated commercial bank branches will then assess the value in line with the above guiding principles. For a list of designated branches, please see Commercial bank PDF.

A banknote is deemed dye-stained when it displays staining patterns from a currency degradation system.

These devices degrade banknotes, making them unusable and discouraging criminals from stealing them. As these banknotes are considered the proceeds of crime, they have no value and cannot be exchanged.

Dye-stained banknotes should under no circumstances be accepted. Members of the public who unwittingly come into possession of these banknotes cannot claim from the SARB, and are advised to hand in these banknotes at their nearest police station.

Examples of dye-stained banknotes:

Currency protection devices (CPDs) protect banknotes from theft by degrading their integrity, making them unusable.

The SARB regulates the use of CPDs in accordance with the SARB Act. Only CPDs or systems that are tested and formally approved by the SARB may be used to protect cash.

All enquires or applications for testing and requests for approval of CPDs, security ink or any other banknote degradation systems must be directed to: CPD@resbank.co.za.

The SARB has the sole authority to produce and issue banknotes and coin. It also has sole discretion to give or refuse permission to reproduce images of its currency.

Entities or persons who would like to reproduce images of the currency can only do so under specific approved circumstances. The images must not be reproduced with the intention of misleading or defrauding the public, and must maintain the dignity of any national symbol.

More details on the guidelines for reproducing banknotes can be found here.

Images in this gallery are available for non-commercial use only. They can be used and reproduced provided the following conditions are met:

The SARB provides support, education and awareness on banknotes and coin to the public.

In collaboration with relevant stakeholders, the SARB runs ongoing public engagement programmes at taxi ranks, malls, schools and community gatherings. The team also conducts public awareness in Common Monetary Area countries, where the rand is legal tender.

Members of the public or organisations who wish to invite the SARB delegates to their area for awareness and training at no cost, can contact us at: +27 12 313 4713 or currency@resbank.co.za.

Most definitely. Members of the public are advised to check the banknote's security features before accepting them.

Like any other surface that large numbers of people come into contact with, banknotes can carry bacteria or viruses. However, the risk posed by handling a banknote is no greater than touching any other common surface, such as handrails, doorknobs or credit cards.

No. The SARB will only accept and exchange South African currency.

No, all circulation R5 coins retain their respective face value of R5 only. The SARB does not buy back currency from members of the public.

No, circulation coins will always retain their respective face value irrespective of their date of issue.

A counterfeit note is an imitation of a banknote produced without the legal sanction of the government. Producing or using counterfeit notes is illegal and a form of fraud.

Such banknotes or coins should be reported to their nearest police station.

No, counterfeit notes have no value and cannot be exchanged for genuine banknotes.

Any information about counterfeit notes operations should be reported to the nearest police station.

A banknote is deemed mutilated when its condition requires special examination to consider the value, if any, to be paid. Such banknotes could be burnt, discoloured, decomposed, damaged with portions missing and/or contaminated.

Mutilated/damaged banknotes can be exchanged at a commercial bank branch where a member of the public holds an account. Alternatively they can be exchanged at the SARB Head Office during weekdays.

Yes. All reproduction images of South African currency should be approved by the SARB before use.

No. Approval of reproduction is granted for a particular period only.

Yes. All approved reproductions should reflect the word “SPECIMEN” on them.

When the Reserve Bank issues a new series of banknotes, the previous issues remain legal tender but are referred to as “old” series banknotes.

At the designated commercial bank branch where an individual’s account is held or at the SARB Head Office in Pretoria.

No. Old series banknotes retain their respective face value and cannot be sold for a higher value.

Dye-stained banknotes are banknotes that are stained by permanent inks used in currency protection devices to secure banknotes in automated teller machines (ATMs), safes and during transportation of cash.

When a banknote is stained by the activation of the currency protection devices, the staining ink penetrates the banknote and leaves traces which are normally more pronounced on the edges of the banknote and in some instances the banknote is completely saturated by the staining ink.

No. These banknotes are not fit for circulation and they will not be replaced for value.

If the dye-stained banknote came from an ATM, you must immediately report it to the relevant bank.

You should always refuse to accept dye-stained notes and notes that are not whole. Only accept clean banknotes and banknotes that are not damaged.